Is India Entering an External Balance Crisis?

On May 10, 2026, Prime Minister Narendra Modi of India made an unusually direct public appeal for restraint: cut fuel use, avoid unnecessary foreign travel, reduce gold buying, and conserve foreign exchange. The message immediately raised a bigger macro question: is India entering an external balance crisis?

The backdrop explains why the speech mattered. A severe West Asia energy shock pushed oil prices sharply higher, widened India’s import bill, and drove the rupee to repeated record lows. India remains a fast-growing economy with large reserve buffers, strong services exports, and a still-manageable macro position, but it is also deeply exposed to imported energy and vulnerable whenever crude prices surge.

That means both things can be true at once. India is under real pressure, and policymakers are responding seriously. But that is still not the same thing as saying India is on the verge of a 1991-style balance-of-payments breakdown.

TradeX view: India is in an external-balance defense phase. The right framing is serious stress, not imminent collapse.

What Happened

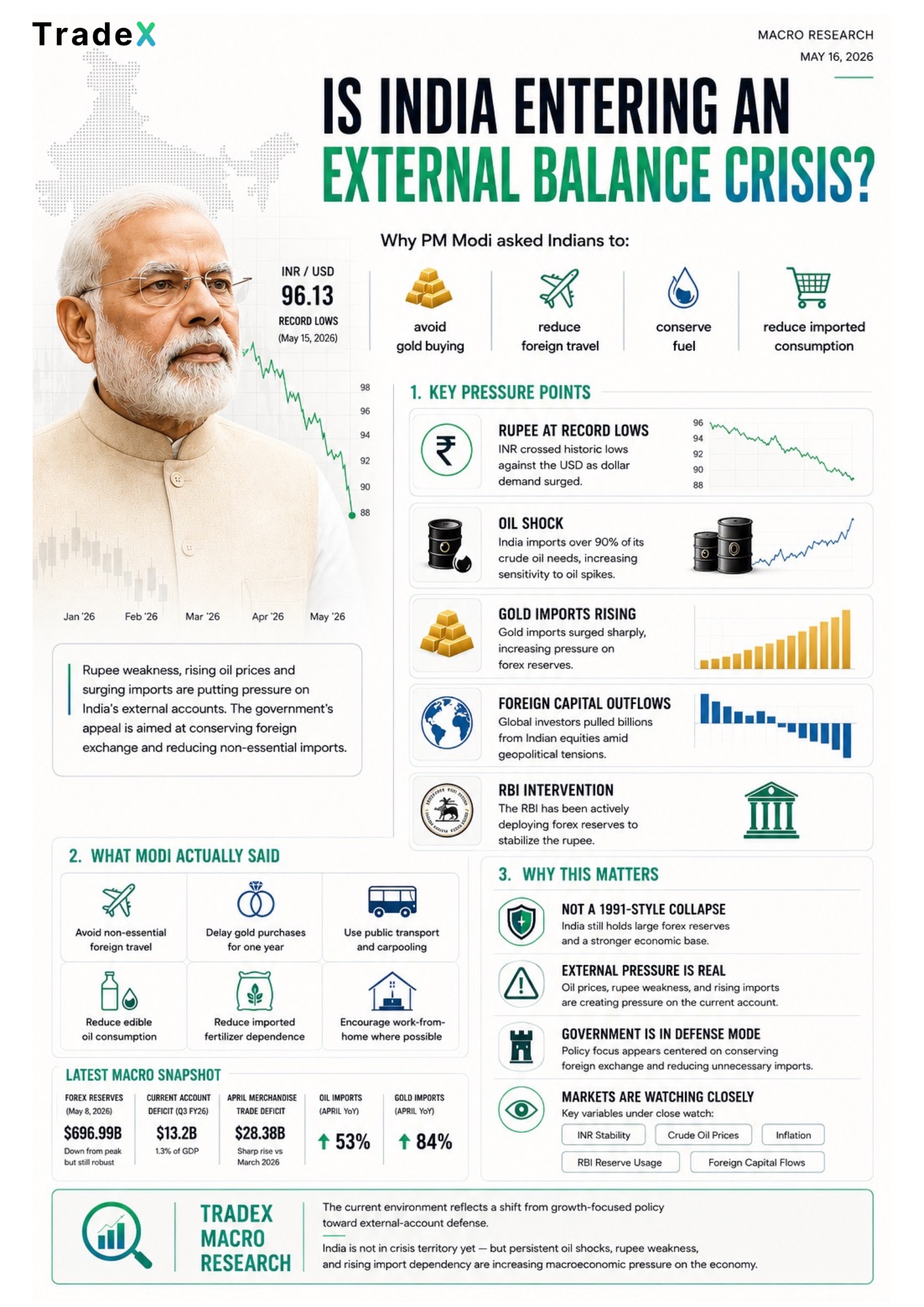

The chain of events is relatively clear. Oil prices surged after the West Asia shock deepened, shipping and supply risk around the Strait of Hormuz intensified, and India’s import-heavy energy profile quickly turned into a currency problem. As the import bill widened, the rupee weakened sharply, foreign portfolio outflows added pressure, and the RBI had to lean on reserves and market controls to keep moves from becoming disorderly.

That is the context in which Modi spoke. His remarks were not a sudden moral lecture detached from markets. They were a political signal that the government wanted households, businesses, and state institutions to reduce discretionary dollar usage while official agencies managed the energy and currency shock.

What Modi Said, And What He Did Not Say

Modi’s appeal was built around conservation and economic self-reliance: use public transport, avoid unnecessary foreign travel, reconsider destination weddings abroad, cut back on gold buying, reduce edible-oil consumption, and lower dependence on imported fertiliser inputs. The intent was clear: conserve foreign exchange while the country absorbs a higher oil bill.

Just as important is what he did not say. He did not announce a travel ban, formal capital controls, or a legal emergency regime. Later public clarification rejecting reports of outright travel restrictions reinforces that distinction. This was moral suasion and administrative tightening, not a full coercive-controls announcement.

What The Indian Economy Looks Like Right Now

India’s macro picture is mixed, not broken. Growth remains relatively strong compared with most major economies, services exports still cushion the external account, and reserves remain large by historical standards even after intervention. Those are genuine strengths.

At the same time, India imports the vast majority of its crude needs, remains sensitive to commodity inflation, and cannot treat a weaker rupee as a clean export-positive story in the way some manufacturing-heavy economies can. When energy prices surge, India feels it through trade, inflation, the current account, and the currency all at once.

Snapshot

What Matters Right Now

| Signal | Latest Read | Why It Matters |

|---|---|---|

| Rupee stress | Past 96 per USD | Successive record lows show the pressure is real and not just a headline effect |

| Oil dependency | More than 90% of crude imported | Higher oil feeds directly into India’s import bill, inflation pressure, and current-account strain |

| April trade gap | $28.38B merchandise deficit | Confirms that the energy shock is now visible in official trade numbers |

| FX reserves | $691B–$697B range in early May | Reserves are down from the peak, but still far larger than in any true crisis-period comparison |

Modi’s Austerity Appeal, In Practical Terms

Modi’s remarks in Hyderabad were framed as appeals for economic self-reliance, but the practical message was conservation. Households and institutions were encouraged to cut discretionary foreign-exchange use and reduce imported consumption while the country absorbs the oil shock.

Modi’s seven practical appeals

Lower fuel consumption was the most direct part of the message, aimed at easing pressure from imported energy costs.

The point was not a legal ban. It was a public appeal to reduce discretionary dollar outflows.

This was a symbolic but targeted signal against visible non-essential foreign spending.

Gold is culturally important, but from a macro perspective it is one of India’s largest discretionary imports.

Less commuting means lower fuel demand, which matters more when crude is above $100.

This reflects concern about imported food and household-input dependence, not just transport fuel.

The goal is to reduce agricultural vulnerability to currency weakness and external supply disruptions.

He did not announce formal capital controls or a travel ban. In fact, he later publicly rejected those rumors.

Why India Is Under Pressure

The immediate driver is West Asia. As oil prices surged and the Strait of Hormuz became more fragile, India’s import dependence turned into a macro vulnerability. Because India imports the overwhelming majority of its crude needs, every move higher in energy prices hits the trade balance, inflation expectations, and currency stability at the same time.

April’s official trade data made the pressure visible. Imports rose sharply, oil imports jumped, and gold imports surged as well. At the same time, foreign capital outflows, importer hedging demand, and overseas debt repayments added to dollar demand. In simple terms, more dollars were needed at the exact moment more dollars were leaving.

India’s current pressure begins with imported energy. Higher oil widens the deficit faster than currency weakness can help exporters.

This is not only an oil story. Gold, non-petroleum imports, and essential inputs are also keeping dollar demand elevated.

Foreign investor selling and importer hedging demand have made it harder for the rupee to stabilize naturally.

Record lows do not automatically mean collapse, but they do confirm that India is under meaningful external stress.

What The Government And RBI Are Doing

The state response has not been one single dramatic measure. It has been layered. First came fuel-security management and logistics support. Then came RBI defense against disorderly currency moves. Then came the public conservation signal from Modi. After that came additional steps such as higher gold and silver import tariffs and fuel-price pass-through.

This pattern tells us something important: policymakers are not waiting for a full-blown crisis. They are trying to slow non-essential dollar leakage, manage expectations, and buy time while external conditions remain hostile.

Is This A 1991-Style Crisis?

Not at this stage. That is the most important conclusion from the report. India is under stress, but the macro starting point is far stronger than the one that existed in 1991.

Reserves remain very large by historical standards. Services exports still cushion the broader external account. GDP growth is slowing only modestly, not collapsing. And the government still has room to manage through reserves, tariffs, logistics, and administrative tightening.

The real risk is continued depreciation, not immediate collapse. If oil stays above $100, foreign capital keeps leaving, and demand adjustment remains slow, the rupee can weaken further even without a 1991-style breaking point.

What This Means For The Economy

The first transmission channel is imported inflation. A weaker rupee makes oil, fertiliser, edible oils, and industrial inputs more expensive. That cost pressure eventually moves through freight, food, chemicals, household budgets, and corporate margins.

The second issue is composition. India is not a classic exporter that benefits cleanly from currency weakness. Because it remains a large net importer of energy and key inputs, a weaker rupee often creates more pain than advantage.

The best interpretation of Modi’s message, then, is not panic. It is preparation. The government is signaling that India should temporarily shift toward conservation while the state manages fuel security, import compression, and rupee stability behind the scenes.

TradeX Perspective

For markets, this matters in three ways. First, India remains highly sensitive to crude. Second, INR pressure can become a proxy signal for broader emerging-market vulnerability if oil stress persists. Third, the policy response shows how quickly governments can pivot from market reassurance to conservation messaging when external balances come under strain.

That makes this a research story worth watching beyond India alone. It is a live example of how energy shocks travel through currencies, trade balances, reserves, and domestic political communication all at once.

Conclusion

India is not facing an imminent 1991-style collapse, but it is facing a serious external-balance test. Modi’s austerity appeal reflects that reality. The country is using moral suasion, targeted import discouragement, reserve management, and fuel logistics to protect macro stability while the oil shock plays out.

The right read is not complacency, and it is not hysteria. It is that India is under real pressure, but it is managing that pressure from a much stronger starting position than the panic narrative suggests.